2024 Housing Market Outlook

Though things are looking up, it’s not too hot, not too cold, but not quite right either

By Mark Fleming

By Mark Fleming

The housing market has been on quite the roller coaster ride since the beginning of the pandemic. While it was strong before 2020, the onset of the pandemic and the societal changes it triggered redefined the role of a home. As work-from-home became the new normal, a house was no longer just a dwelling or a vehicle for wealth creation, but also an office, a classroom, a daycare and even a gym. The broadening role of the home in American life, in conjunction with record-low mortgage rates, powered the housing market to multiple records during this unprecedented time – the fastest annual house price appreciation, the lowest days on the market and a near-record pace of sales.

Yet, the housing market’s frenetic pace was unsustainable in the long run, so what went up so quickly, had to come down. In response to fast-rising inflation, the Federal Reserve reversed its easy money policy and embarked on the most aggressive monetary tightening since the early 1980s. Mortgage rates increased sharply as a result. With mortgage rates and home prices both high, and inventory limited, one couldn’t buy what’s not for sale and, in many cases, couldn’t afford it either. Home sales in 2023 dipped to the lowest levels in over a decade. While 2023 represented the housing market roller coaster’s descent to the bottom, 2024 is likely the flat stretch representing the calm coast before the next ascent.

Mortgage Rates – Higher than the Goldilocks Rate

The outlook for the housing market in 2024 is heavily dependent on the path of inflation and the health of the economy. The Fed’s projections indicate that their battle with inflation could end soon, which means we may not see any more interest rate hikes. Mortgage rates have already retreated from recent peaks near 8% and may fall further once the Fed signals clearly that monetary tightening is over.

However, the economy remains strong, so it’s less clear when the Fed may start lowering rates again, what ‘higher for longer’ really means or what the goldilocks (not too hot, not too cold, but just right) federal funds rate level even is for this economy. The most likely scenario in 2024 is that the economy and labor market continue to cool, but not collapse. And, if the Fed’s projections are correct, we may even see one or two modest rate cuts. As the Fed maintains a ‘higher than goldilocks’ stance, mortgage rates likely will also remain high, hovering in the 6.5% to 7.5% range.

2024 Supply, Demand and Prices—Oh My!

You Still Can’t Buy What’s Not for Sale: Assuming that mortgage rates moderate in 2024 from recent peaks, affordability may improve slightly, bringing some buyers off the sidelines. Additionally, lower and more stable mortgage rates may encourage some existing homeowners to sell, but it won’t be enough to meet demand. Existing homeowners remain rate-locked into their homes. This disincentive to sell is likely to persist as long as mortgage rates remain elevated. Only when more homeowners decide to sell, and then buy again, will the housing supply and the pace of sales return to anything resembling ‘normal.’ Homebuilding helps add more supply, but new homes are a small share of the total market, so it is difficult for homebuilding alone to solve the supply problem. Assuming six months supply is balanced and the average pace of sales of new and existing homes combined, is 4.8 million SAAR so far in 2023, then an ideal supply of homes for sale is approximately 2.4 million homes. We are currently about a million homes short. The supply shortage will continue in 2024, as more than 90% of existing homeowners will remain rate locked in at mortgage rates between 6.5% to 7.5%.

Millennial Demand in the Shadows: Today, millennials, the largest generation to date, are aging into their 30s. Additionally, millennials’ higher educational attainment is translating into greater earning power, a strong predictor of homeownership. As of 2022, over half of millennial households were homeowners, which still leaves many more young households who may want to become homeowners. In the short term, reduced affordability and limited inventory may lead them to delay, but not forgo, their transition into homeownership. This millennial ‘shadow demand’ will continue to trickle into the housing market in 2024, as millennials motivated by life changes, such as moving for a job or growing families, purchase homes.

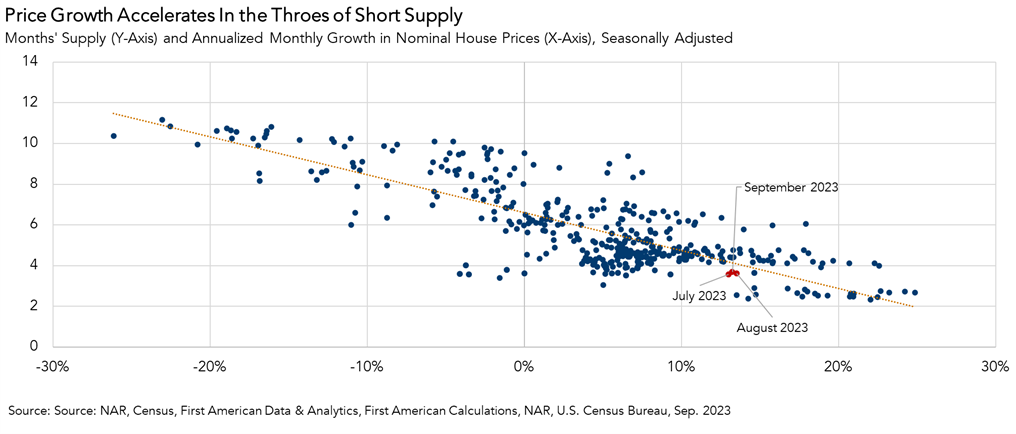

Prices: According to First American Data & Analytics October 2023 Home Price Index, house prices nationally set a new record for the seventh straight month. Potential sellers continue to sit on the sidelines, limiting supply, while buyers who can afford to purchase chase what few homes are available for sale. House price growth and total months’ supply have an inverse relationship. Historically, six months of supply is associated with moderate price appreciation, but a lower level of months’ supply tends to push prices up more rapidly. Total months’ supply in 2023 has consistently remained below four months, putting upward pressure on prices. In 2024, total months’ supply may increase modestly, but it is not expected to get back to ’normal’ unless there is a major shock to millennial demand. Therefore, if this relationship between months’ supply and home prices repeats itself, there will be continued upward pressure on prices to grow faster than normal in 2024.

Too Hot, Too Cold or Just Right?

The housing market pulled forward several years’ worth of demand in just two years from mid-2020 through mid-2022. Now, with affordability and inventory constraints, some demand is being pushed back. 2024 will likely present many of the same challenges the housing market faced in 2023 – higher than goldilocks-level mortgage rates, restricted affordability and a lack of inventory for sale. If the 2020-2021 housing market was ‘too hot,’ then the 2023 market was probably ‘too cold,’ but 2024 won’t yet be ‘just right.’

Mark Fleming is chief economist at First American.