Builders to Benefit From 2024 Affordability Crunch

High mortgage rates and home values strain affordability, but builders, with incentives, are expected to outperform this year

By Alex Shaban

By Alex Shaban

Above 7% mortgage rates and rising home values have created the worst affordability crisis for home buyers in decades. The Fed’s “higher-for-longer” approach to rates and the sheer number of homeowners “locked-in” at low rates suggest that affordability will likely remain stretched throughout 2024. However, this means that builders are well-positioned to outperform the resale market in 2024 as they did in 2023, as incentives like rate buydowns continue to position new homes favorably relative to existing homes.

High Rates Froze the Housing Market in 2023

2023’s housing market was defined by mortgage rates reaching levels unseen in recent decades. Mortgage rates currently stand at 7.2% and have directly impacted affordability by significantly increasing the cost of home ownership. This rise in rates has priced out millions of potential buyers.

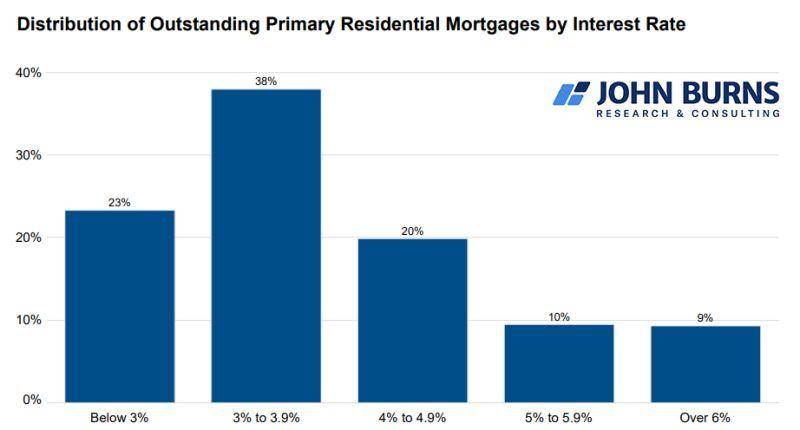

In addition to the impact on buyers, 7%+ mortgage rates have also “locked in” the 80% of existing homeowners with sub-5% rates, since at today’s rates, they would have to settle for a smaller home to keep their payments the same. This strongly incentivizes existing homeowners to cling to their low rates and is also why listing volume has been anemic for much of the year.

The combined hit to both housing demand and housing supply froze the market. Existing home sales fell to their slowest pace since the mid-90s, indicating a market where fewer buyers and sellers are able or willing to participate.

However, buyers continued to outnumber sellers in most markets across the country, which pushed home prices upward. Nationally, home prices increased 5% year-over-year in 2023. Rising home prices, coupled with 7%+ mortgage rates, have stretched affordability to its worst position since the early 1980s. A typical homebuyer today would allocate an average of 46% of their income to housing costs, well above the norm of 32%.

In 2023, builders navigated the market slowdown with notable success, capitalizing on the resale market’s low inventory to divert demand toward new homes. By September, new homes comprised nearly a third of all single-family inventory for sale (completed and under construction). Builders effectively responded to high rates by buying rates down to the 4-6% range and offering a much lower monthly payment than a comparable resale home. This helped new homes account for around 14% of all

home sales by September 2023, the highest share since 2008. Builders were also able to generate healthy profit margins by reducing home sizes while maintaining prices, thus increasing the price per square foot.

2024’s Challenging Affordability Landscape

Expect rates to stay high next year. In their forecasts, Fed officials expect interest rates will still be above 5% by December 2024. The Fed has made it clear that it does not intend to cut rates until inflation is back to 2% growth (PCE was 3.0% as of October), or if there is strong evidence of damage in the labor market. To begin to cut rates before either of these events would be a significant hit to the institution’s credibility.

Despite some recent softening, a still-solid labor market indicates that the Fed is likely to maintain near-current interest rates while inflation is elevated, keeping mortgage rates high. Listings will also likely stay low as the ongoing ‘lock-in’ effect keeps homeowners in place, keeping prices sticky.

Mortgage rates may come down slightly independent of Fed action (for example, if the inflated spread over the 10-year compresses). However, any improvement in affordability is likely to be limited. Even if supply increases as a result of the ‘lock-in’ effect waning at lower rates, a corresponding increase in demand from buyers who had previously been priced out will keep home prices from falling significantly.

In an environment where affordability remains stretched, builders will continue to have an edge over the resale market, as their ability to offer incentives like rate buydowns makes new homes more affordable (and therefore more attractive) than existing homes.

Be Wary of Potential Risks

1) A potential uptick in resale supply could pose a challenge for builders. As time goes on, the lock-in effect will gradually wane. Because demand is so low due to high rates, it will not take a significant amount of resale supply to have a significant negative impact on prices, which would dilute the relative affordability of new construction today. Supply is already rising unseasonably in markets like San Antonio, Houston and Miami, which have all posted double-digit year-over-year increases in resale listings.

2) If mortgage rates stay above 8% for a sustained period, builders’ ability to offer attractive rate buydowns could be compromised. Builders can buy down rates to the 5-6% range, an incentive that the resale market simply can’t match. But at 8%+ rates, builders will have difficulty buying rates down to levels acceptable or feasible for most buyers.

3) While not our base case for the economy, the risk of a Fed-induced job-loss recession still looms as job market indicators begin to soften. A major job-loss recession would drastically reduce the pool of potential homebuyers, weakening the demand for new homes. Employment growth is currently at a healthy 1.9% year-over-year, but a softer-than-expected November jobs report suggests cooling. Job openings and voluntary job quits have also receded from their all-time highs, suggesting waning confidence in the labor market.

Concluding Thoughts

As we move into 2024, the housing market will remain broadly unaffordable for buyers due to high mortgage rates, limited inventory and sticky home prices. The Fed is likely to keep rates “higher for longer,” and the ‘lock-in’ effect will likely continue to weigh on inventory. These factors, combined with steady demand, will continue to support home prices, making significant affordability relief unlikely.

In this environment, builders are set to outperform once again. Their capacity to offer rate buydowns positions them favorably in a market where resale options remain constrained and less appealing. However, builders should remain cautious of risks, particularly on the supply side, given limited demand at today’s rates.

Analysis and column also contributed by Alex Thomas, senior research analyst at John Burns Research and Consulting.

Alex Shaban is a research analyst at John Burns.