Surprising Strength in Housing and Labor Markets

Typically considered rate-sensitive, the housing market has proved to be resilient

By Alex Thomas

The Federal Reserve has raised rates by over five percent since mid-2022. Although housing is typically considered among the most rate-sensitive sectors, the housing market has proved to be resilient.

Specifically, home prices and new home sales have performed much better than would typically be expected during the fastest rate hike cycle in decades. Our outlook for 2023 and 2024 is “cautiously optimistic.” And although the impacts of inflation and rising interest rates are top of mind, there are some green shoots for housing.

Demand remains strong for both for-sale and rental housing (single-family rentals more so than apartments), with a surge in demand in the spring 2023 selling/leasing season, after a sluggish end to 2022. Inventory also remains near historic lows as homeowners cling to their low mortgage rates, which is keeping prices steady or rising.

Work-from-home has permanently and positively impacted housing demand and productivity in most markets. The ability of fully remote workers to relocate and for hybrid workers to live further from the office has helped address the major affordability challenges posed by the rapid rise in home prices and mortgage rates.

Homeowners are in great financial shape. Home equity has exploded, with household balance sheets in the strongest position seen in recent history. Nationally, the economy has been resilient. The labor market is still on fire. The economy is continuing to add hundreds of thousands of jobs each month, and the gap between labor demand (number of employed plus job openings) and labor supply (labor force) is higher than it’s ever been—signaling a tight labor market and competition for labor.

No early warning signs of labor market distress are flashing. Jobless claims (the number of people receiving unemployment benefits) are still extremely low by historical averages and show no signs of increasing.

Even the most “rate-sensitive” sectors like tech, finance and housing continue to exhibit demand for labor. Tech was arguably hit the hardest earlier in the year, but reports of mass layoffs have slowed, and AI fervor has breathed life back into the sector.

Employers are still actively looking to hire at/or near record levels. Job openings have fallen from all-time highs, but still far exceed pre-2020 levels.

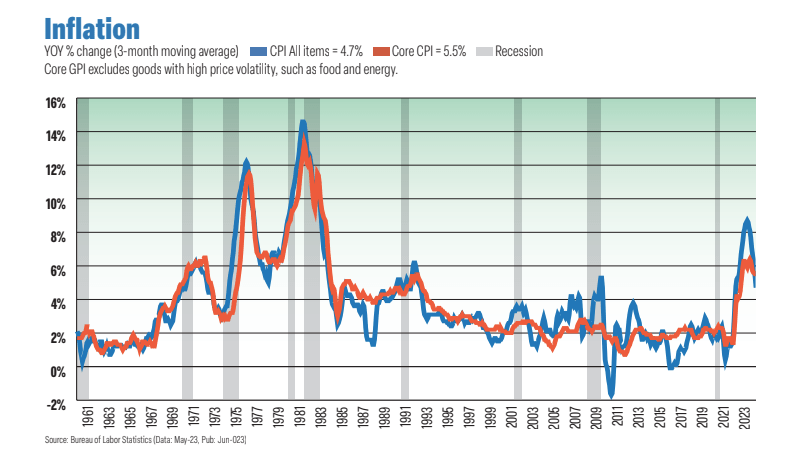

Inflation, which typically eats at consumers’ wallets, has cooled to approximately four percent. Consumer expectations for inflation have also come down—signaling rising consumer sentiment. Wage growth remains strong across the board. Stock prices surged in 2023 after sharply falling in 2022.

Builders have several reasons for optimism: on the homebuilder front, the homebuilder market share will continue growing for big homebuilders. Even as rates spiked to approximately seven percent, demand for housing continued throughout the first half of 2023, helped by very low resale supply and builders utilizing rate buydowns.

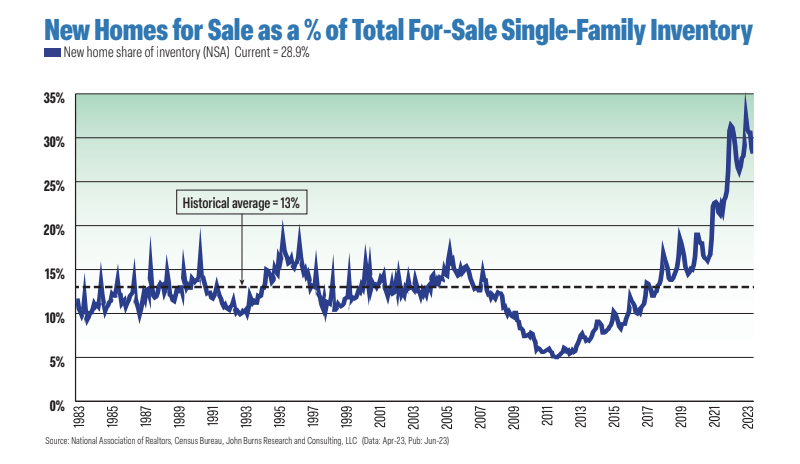

Builders benefit from historically low resale supply as the lock-in effect takes hold. Homebuilders are also successfully stepping into the supply void, adding communities and drawing buyers to the new home market. Homebuilders now offer 29 percent of all the homes available to buy in the country, versus a historical norm of 13 percent.

Builders are quickly bridging the affordability gap thanks to a combination of pricing and financing sales tools (namely rate buydowns undercutting resale sellers), finding the payment sweet spot for many homebuyers.

Fundamental risks and factors we are monitoring that could impact the economy and demand for housing include the Fed’s higher-for-longer interest rate plan, which continues to weigh on banks (namely regional banks) and the availability of consumer credit, and federal student loan payments, which resume in September after three years of being on pause. This will likely pull money out of the economy and possibly suppress entry-level home purchase activity.

Analysis and column also contributed by Danielle Nguyen, vice president of research at John Burns Research and Consulting.

Alex Thomas is a senior research analyst at John Burns Research and Consulting, focusing on tracking macroeconomic trends and analyzing housing market data.